Ticker: UVE

Stock price at the time of writing $ 13.6.

0 Introduction

Property and casualty insurance sector isn’t necessarily one of the hottest places to invest your money right now. Despite the fact, that’s where we are diving into in this stock analysis.

Florida is the third largest property insurance market in the United States. The size of the market is approximately 57 billion dollars and there are around 60 companies serving it. Many large companies left the state after the big hurricanes in 2005 and have not returned since. It’s not only the hurricanes that trouble the insurers of Florida.

In 2019 the insurers in Florida reported $3 billion law-suit related expenses. At least we will know who’s getting rich if it’s not us! Following quote introduces us to the legal challenges in Florida:

“They [insurers] are also facing what McFaddin described as “out of control” litigation in Florida, partly because of a law that can require insurers to pay attorneys “excessive fees” in those cases. The practice has spurred a cottage industry of contractors and lawyers who sue insurers to replace a whole roof when only a few tiles are damaged, insurers say.

Other less dramatic problems, such as leaky pipes, happen at an “abnormally high” frequency in Florida, often causing severe damage, including mold, consistently gnawing at profits, said Charles Williamson, chief executive officer of Vault, a Florida-based insurance exchange for wealthy individuals.” (Source: Insurance Journal)

Extreme weather and high litigation costs have made Florida nearly a rogue state when it comes to homeowner insurance business. Insurance prices are now rapidly rising, some insurers are reducing their business in Florida and lawmakers have woken up to the issues in the industry. Additionally, the stock prices of the insurers that are still left have been battered. Interestingly, the ongoing changes in the market, low valuations and improving finances bring these insurers to our attention. Can we find a value, low-risk and high-reward type of a situation, where a nimble investor could make a decent profit and pocketing a dividend while waiting things to play out?

Now let’s take the framework and take a look at the largest P&C insurer in Florida, Universal Insurance [in short Universal].

1 Company

Business

Universal Insurance is a holding company founded in 1990 and operating primarily in the state of Florida. It operates under different brands to serve the complete value chain, primarily focusing on homeowner insurance for households. Universal holds a market leading position in the Florida market with 10-11% market share. Company employs approximately 900 people.

Universal’s business can be divided into three parts:

Underwriting

Services

Investments

Underwriting business can be measured by two numbers: number of policies and amount of premiums in force. Number of policies is nearing 1 million and it has grown at 9.5 % CAGR. Amount of premiums is approximately 1.5 billion and it has grown at 11.4% CAGR. Universal collects 82% of its premiums in Florida and the rest out of the 18 other states and two licenced states. Five years ago other states represented only 5% of the total.

Universal distributes its products through 10 000 independent agents, Universal Direct and its own Clovered.com portal. Clovered also represents other insurance companies and consumers can compare and buy different types of insurance online. Unfortunately, it is relatively difficult to evaluate how popular the site is. During the months Jun-Sep 2021 the site had 15 000 visits on average per month, which seems to be a rather low number. In the Q2 earnings call, the management gave a number of 40 million in written premium without specifying the time frame in which that was generated.

Services consist of several different business lines. In 2020 it generated $65.4 million of revenue (6% of total), which consisted of risk management commissions (51%), MGA policy fees (36%) and other (13%). MGA generally means underwriting, settling claims, pricing, and binding risk on behalf of an insurer. Services have grown impressively at 12.5 % CAGR for the past five years. Universal includes Clovered.com under services.

At the end of the second quarter Universal's investment portfolio was 1 billion dollars, consisting of corporate bonds (53%), mortgage-backed and asset-backed Securities (31%) and other investment vehicles. Investment returns naturally play an important role in the financials of an insurance company. Last year Universal saw a drop of net investment income from $30 million in 2019 to $20 million in 2020. The decrease was driven by lower market yields.

Management

Management owns approximately 10% of the outstanding shares. Last time management increased its ownership was in November 2020 by Sean Downes, executive chairman of the board and former CEO. In the past, he has been an avid trader of the stock. In 2021 he conducted regular sales of blocks of 20 000 shares per month and in total approximately 90 000 shares at an average price of 14 dollars. According to TIKR he still owns 1.5 million shares, making him the 4th largest owner of the company, 4.6 % of outstanding shares. CEO Stephen Donaghy holds approximately 600 000 shares and chief risk officer Jon Springer holds around 500 000 shares.

Mr Donaghy has held the CEO position since July 2019 being promoted internally from the COO position. Donaghy’s salary in 2020 was $ 2.8 million. Former CEO Sean Downes seems to be still quite handsomely compensated for his efforts, whatever they are, pocketing $ 2.5 million in base salary and options in 2020. In 2019 he made a whopping $5.4 million. Extravagant compensation in times of trouble definitely raises some concerns. For example, CEO of Donegal, an insurance company of similar size, made $1.3 million in 2020.

According to Glassdoor 91% of 75 reviews “approve” the CEO and 80% would recommend Universal to a friend. Also 78% see a positive business outlook. Overall, employee reviews on Glassdoor are positive, especially remuneration is highly appreciated.

Financials

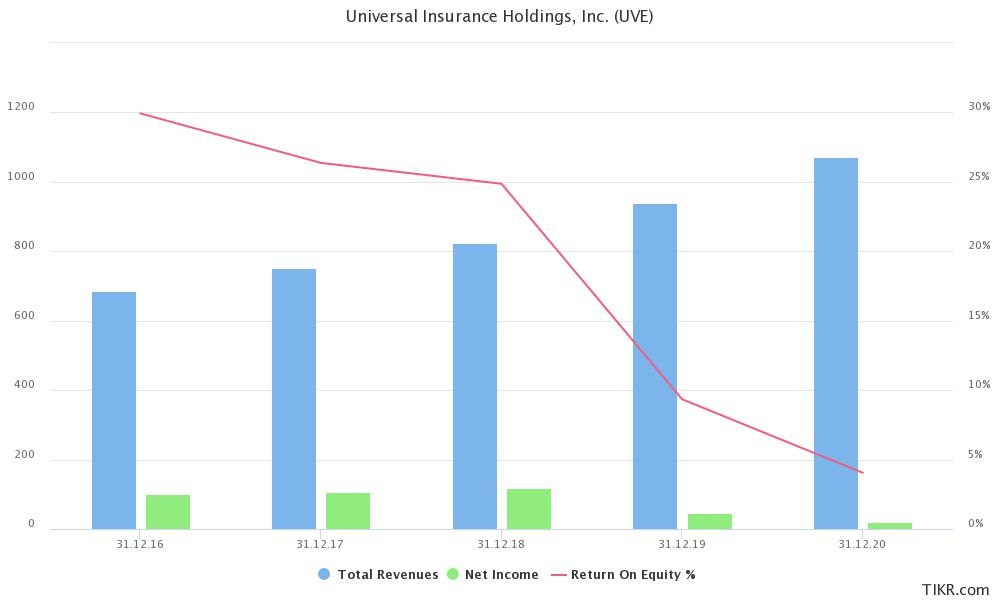

When we look at the financials of the past two years we will understand why the stock price is depressed. Due to major catastrophes (in particular hurricane Irma), excessive litigation, contractor schemes and increasing cost of reinsurance, Universal and other insurance companies in Florida have delivered poor numbers. In 2020 Universal reported $ 162 million impact after reinsurance. These conditions have meant that while Universal’s revenues have been steadily climbing, its results have dropped down the cliff.

“Everybody has seen loss creep in their books over the last three years that no one expected.”

According to Insurance Journal the situation in Florida has been improving from 2020. The financial impacts of claims and litigations from hurricane Irma are finalized. In the first half of the year Universal has got itself back to green numbers. Its combined ratio was 93,1 % in Q1 and 97,3 % in Q2. Year by year Universal has been able to decrease its G&A costs in relation to premiums. Together with high growth numbers and lower expenses Universal has been guiding towards $ 2,75-3,00 EPS. Diluted EPS for the six months ended June 30, 2021 was $1.54 compared to $1.23 in 2020, an increase of $0.31, or 25.2%.

Universal is currently carrying very little debt in its books, less than $8 million. If a catastrophe size storm hits Florida, Universal possibly could take on debt to sustain the bad times. Historically Universal has delivered high return on equity. Its five-year average stands currently at 18,5% that has been elevated by low reinsurance pricing and mild weather in some years. In Q1 and Q2 Universal reported ROE of 23.2% and 18.7% respectively.

Universal has been a steady grower of revenues and premiums. This trend continued in the first half of 2021. Total revenue was up 11,7% in Q1 and 10.1% in Q2. The written premiums grew 9.2 % in Q1 and 17% in Q2. Also, the book value of the company saw a small uptick during the first half year and the company holds a large cash position, which sets the enterprise value extremely low.

Competition

The company itself describes the market of homeowners insurance as highly competitive. Furthermore the company states: “The personal residential homeowners insurance industry is strictly regulated. As a result, it is difficult for insurance companies to differentiate their products, which creates low barriers to entry (other than regulatory capital and other requirements) and results in a highly competitive market based largely on price and the customer experience.” In 2020 the company’s renewal retention rate was 89%. This compares rather well to the industry standards.

Universal has several local competitors. United Insurance Holdings (UIHC), Heritage Insurance Holdings (HRTG), FedNat (FNHC) and state-owned Citizens. Going through the latest financials of some of the competitors, it appears that Universal has fared better overall than its stock-listed rivals. See valuation section for comparison of valuation multiples.

How does the company fare against the competitors pricewise?

According to the review by Nerdwallet.com from July 2021, Universal Property positions itself in the higher price range out of a sample of 15 insurance companies.

According to Valuepenguin.com Universal is among the 10 cheapest home insurers in Florida holding 8th position.

Key figures

Revenue 2020: $1072.8 million

Revenue 2021, estimate: $1100 million

EPS 2020: $0.47

EPS 2021 guidance: $2.75-3.00

ROE 2021 guidance: 17-19%

2 Dividend

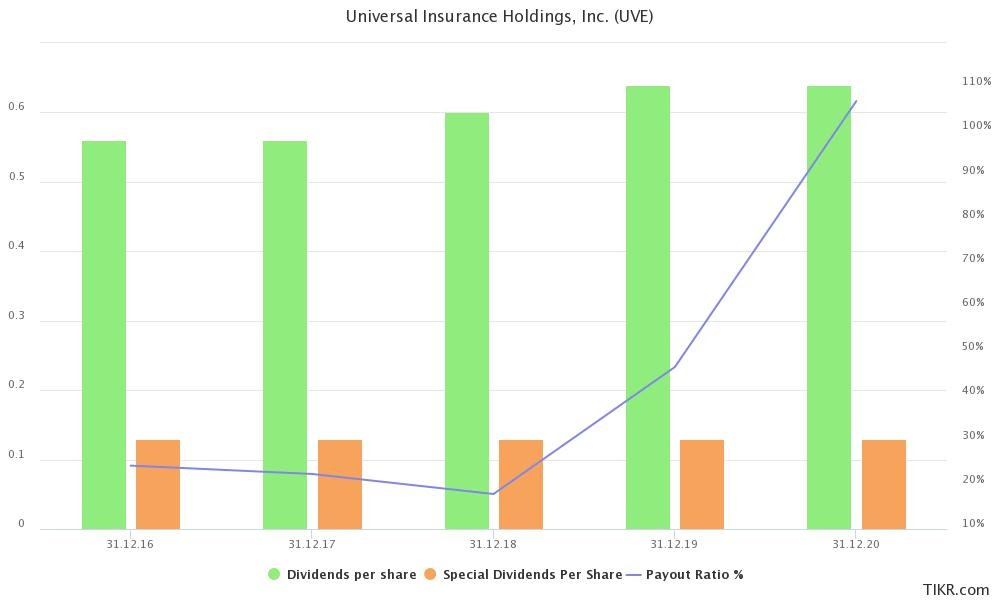

Last year Universal paid a regular dividend of 64 cents. Company has been paying a quarterly dividend for 8 years. The dividend has been trending higher and there’s been only a couple of years (2017 and 2019) when the company has decided to maintain the dividend at the same level as previous year. Current dividend yield stands slightly below 5%, which is significantly higher than the four year average of 3.5%. For many years Universal has paid an additional fifth instalment in the last quarter. In 2020 and previous years the company paid $0.13 special dividend on top of the regular dividend. This would boost the yield even further.

The current pay-out ratio stands at around 27% if we use the estimated EPS $2.4. If the company can meet its FY21 EPS guidance of $2.75 - $3.00, the pay-out ratio would be only 23 to 21 per cent.

According to the investor presentation, during the last five years the company has bought back more stock than paid dividends ($147 million vs. $124 million). At the moment Universal has three authorized programs to purchase $100 million worth of stock. Two of these programs, $80 million, will expire by the end of 2021. During the first half of the year Universal only bought back 15 444 shares.

Key figures

Dividend yield: 5-6%

Payout ratio: 27%

Dividend CAGR 5Y: 4.2%

3 Valuation

Key figures

MCAP: $430 million

FWD P/E: 5.6

Current P/E: 15 (5Y avg 13.44)

Current P/S: 0.37 (5Y avg 1.09)

Current P/B: 0.86 (5Y avg 1.83)

ROE 2020: 4.1% (5Y avg 18.5%)

Simulation

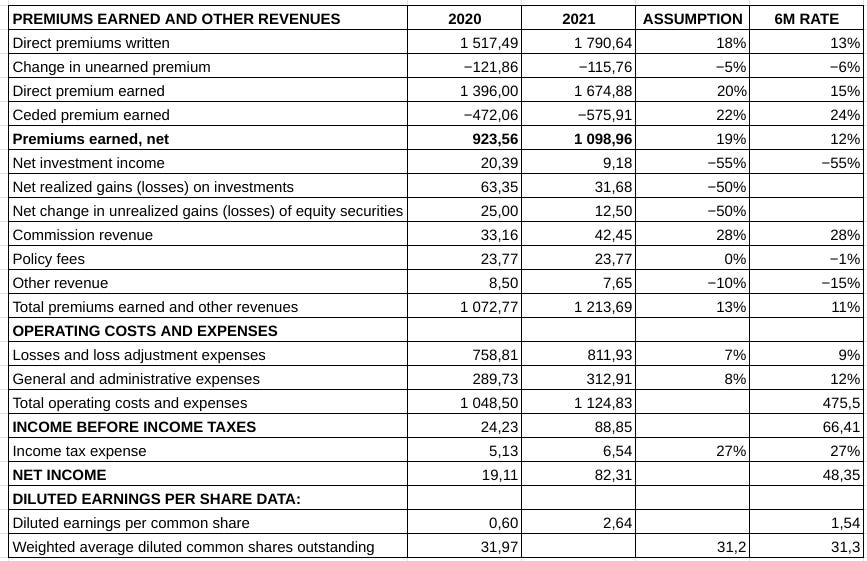

Key figures look tempting for a (deep) value investor. Whether Universal is cheaply valued or not, depends in large part on the likelihood of delivering strong numbers in the coming quarters. What kind of numbers would Universal need to deliver in 2021 in order to reach a historically normal level of EPS? In the table below we first take numbers of 2020, then first 6 months of 2021 as a guiding rate and last, make an assumption what could be realistic development of the financials. We reach an EPS $2.64, slightly above analyst estimates and slightly below lower range of the company’s guidance.

Key assumptions are that the company's sales growth accelerates, growth of losses decelerates, growth of G&A expenses decelerates supported by the catalysts [see section catalysts]. Higher insurance pricing, lower litigation costs and lower amount of claims being the main drivers. The highest uncertainty there’s with the investment income. In the calculation we assume them to significantly decrease [see section risks]. Assumptions don’t need to be overly optimistic in order to reach EPS $2.64 but it’s rather difficult to reach the level that management is guiding for. If the direct premiums written would increase by 20% and expenses would be only 2 %-points higher, the EPS could reach $3.00.

Peer evaluation

How does Universal’s valuation compare to its peers? Heritage Insurance Holdings has done the heavy lifting for us in its quarterly report. We can see that Universal is valued in a balanced way. Low forward P/E multiple combined with modest, and historically low, P/B, while enjoying relatively high ROEs even during troubled times. The valuation, in combination with financial performance, fares well among the peers, appearing like the most punished stock in the peer group. Universal has one of the highest exposures to Florida market ( e.g. UIHC 67%, HRTG 51%).

Heritage Insurance also gives reasoning why the industry in Florida has seen poor finances during the past years.

(Source: Heritage Insurance Holdings, Q2 2021 presentation)

4 Potential for capital gains

Considerations

Even though every tropical storm is an isolated event, as time passes by it becomes more evident that a storm will cause Universal disproportionate amount of claims. Therefore, Universal might be more of a short or mid term play than a long term hold. Climate change will not help to reduce weather related events.

Due to the unfavourable market dynamics and weather events, the company has delivered poor financials in the past year or two. Before we see some evidence of a chance, the company deserves lower multiples. Fortunately, there’s lurking numbers and fundamentals that could represent evidence about a turn in the performance.

Who will be the buyers of the stock? A small cap stock in a troubled part of an unpopular sector probably will not attract main street investors. If the company continues delivering earnings surprises, the stock might be first discovered by traders and value and dividend investors.

In August, deep-value investment management firm Donald Smith & Co opened a position of 366 000 shares in the company.

Can we or can we not value Universal at its historical average multipliers? If we assume the last five years includes two poor years and three good or normal years, using five year averages would be rather fair.

By giving an ambitious EPS guidance, the management of the company seems to be optimistic about 2021. In estimation of the price appreciation potential, we need to leave out the possibility of accounting tricks and believe in the integrity of the management, which has a significant stake in the company.

Potential

Last time, in 2016-2017 when Universal was reporting $2.5 to $3.00 EPS, the share was trading between 16-30 dollars. However, those years Universal enjoyed much higher ROE (25-29%), whereas currently management expects ROE to reach 18%.

If we take the 5 year average P/E of 13.44 and $2.75 EPS guidance by the company we would be looking at a stock price of 37 dollars. If we apply a 20% safety margin we get a price of $29.6.

If we take the 5 year average P/S of 1.09, first two quarters and estimate sales for last two with 10 % growth rate, we get sales of 1067 million dollars (Q1 260 + Q2 280 + Q3* 256 + Q4* 271 = $1067 million). Then we would be looking at a market cap of $1163 million versus the current $406 million. The stock would need to almost triple to reach that number, meaning 13.6x2.7*0,8= $29.3, assuming again 20% safety margin.

At the end of the second quarter, the book value of the company was $ 15.37. If we multiply it by the 5 year average, we arrive at a stock price of $28.12. Okay, let’s use the same 20% safety margin, so $22.5.

Technically the stock appears to be forming a one year long base in the 13-16 dollar range with the longer moving average starting to flatten. Breaking out above $14.7 could potentially signal a new uptrend.

Finally, let’s take the $2.64 EPS that we came across in our simulation above. Let’s also take the current average P/E of the peer group, 11. By these two figures we arrive to a price of $29. Deducting 20 % safety margin would give us a figure $ 23.2.

The average of above estimations, including 20 % safety margin, is $26.1, meaning a nearly 100% upside to the stock. If we consider the lower level of ROE, a larger safety margin could be applied.

What’s the downside? Are all the bad things already priced in? A new major hurricane probably isn’t, however a good period of strong finances, combined with even a partial tailwind from the following catalysts could also mean a strong uptick of the share price. Strong balance sheet, already depressed valuation and two good quarters in 2021 help to protect the downside.

5 Catalysts

Costs and prices

For a long time the Florida insurance market was suffering from fraudulent claims. For example, a contractor could show up on a property, ring the doorbell, ask if he could inspect the roof, and get the complete roof renewed at the expense of an insurance company. However, that's about to change. Since the 1st of July it has been more difficult to sue insurance companies and new legislation prohibits contractors from doing immoral marketing. Legislative changes could mean that in the future we see a reduced amount of claims and litigation costs. Since the legislation is new, it is yet unclear how the changes will impact the industry.

The past litigation costs and changes in the legislation have led to steep increases in policy pricing. Depending on the insurer, these increases have been in between 10-20% or even more. Some industry incumbents believe that elevated pricing will continue until 2023-2024. Universal was approved for a 12.4% rate increase in May 2020 (July 2020 for renewals) and in December 2020 for a 7% increase (March 2021 for renewals), totalling a 20% increase (100*1.124*1.07=120).

The high costs of doing business in Florida has left many homeowners without renewal of their insurance as insurance companies, for example FedNat, have been reducing their books. The growth of United Insurance was significantly lower in the latest quarter than the one of Universal’s. In the latest Q2 earnings call the management of Universal also highlighted their efforts to have stricter claim handling and underwriting.

Let’s speculate about the weather. No big storms in 2021 in Florida? According to the Florida Climate Center the peak hurricane season occurs between August and October. So far there has not been a major hurricane landfall in Florida. The insurance companies have communicated about softer weather conditions compared to the previous year. Statistically there’s a 45% chance of a hurricane landfall, however the state saw nearly a decade long mild conditions before 2016-2017. If Floridians are spared from hurricanes this year, losses of troubled insurers would be significantly reduced.

(Source: United Insurance, investor presentation)

Growth in other states and buy-backs

For many years Universal has expanded its geographical presence, adding operations into a new state every year. The size of business in each state is relatively small, it looks like Universal is steadily growing organically in each state through agents and Clovered.com. This is a low-risk and low-cost strategy. The company does not need much extra staff to serve these new markets. However, according to the management agency commissions in other states are mostly higher than in Florida.

If the company continues to succeed in the expansion, it will reduce Florida-related risks and grow top and bottom lines. Being less dependent on Florida will most likely help with increasing interest from investors. There’s also a concern. Based on the reported numbers, there’s a possibility that growth in other states is slowing down since the past two quarters the growth has been significantly slower (in average 4% vs. 18% in average in the preceding four quarters).

Are there any other catalysts? There are not many analysts following the company, however Universal has beaten the estimates in the past three quarters by over 15 per cent. As mentioned, the company has used its authorization of stock repurchases. In an extreme case the remaining $100 million authorization would reduce outstanding stock by 25%. The $20 million authorization expiring in 2022 would reduce outstanding stock by 5%.

To sum it up, there’s two significant catalysts for increasing revenues and two or three catalysts for reducing costs. If the catalysts are realized, in full or in part, they will help the company, considering continued organic growth, to exceed market expectations, especially if the company decides to boost per share numbers by buy-backs.

6 Risks

Without question the largest risk for Universal is a catastrophic event, namely a hurricane that sweeps over densely populated areas. What’s the probability of such an event? Statistically it is high, but natural events don’t follow statistical probabilities.

The total insured value and premiums have steadily grown at a double-digit pace. The question that needs to be asked is, if Universal has acquired/sold the insurance policies with a large enough safety margin? Luckily the chief risk officer possesses half a million shares of the company. However, the concern here is that TIV (total insured value) has increased more rapidly than premiums (14.8% versus 11.4%, 5 year CAGR). Has Universal taken too much or more risk on board than it has charged its customers?

One of the aims of recent legislative changes, decrease risk and costs of litigation, was to help more insurance companies to enter Florida by making the cost of doing business more transparent. It remains to be seen if larger companies will enter P&C market in Florida.

Increasing insurance prices leads home owners to purchase their insurance from state owned Citizens Property Insurance Corp. that insures high-risk customers that can not obtain insurance elsewhere. CPI has underwritten an increasing number of new insurance policies growing in double digit numbers (+23% more policies than previous year). It’s probable that this has happened due to the fact that the price increases of private insurers have been higher than what CPI has been allowed to do.

It appears that smaller insurers are rapidly losing market share. For example FedNat reported a decrease of -21.7% of Florida homeowner insurance policies.

In the first six months of 2021 the amount of policies in force of Universal slightly decreased (-0.8%) due to the management’s effort to limit new exposure

Investment income, assuming $20 million net investment income and EPS of $2.75, represent around 1/4 of Universal’s result. If investment income drops, let’s say, to a level $15 million, slightly above 2017 level, it will reduce Universal’s result by 5%. In Q1 and Q2 investment income decreased in total $7.15 million.

In Q2 Universal sold a large part of its investment portfolio and expects the investment returns to be lower in the future.

There are several cost elements that will partially offset the benefits of price increases. In the first six months of 2021 reinsurance costs of Universal increased from 32.6% to 35% of earned premiums. Reinsurance costs typically rise before the primary rate increases. Also, wage inflation and construction material price inflation will have an effect on Universal's cost base.

One major risk is the time component. In what time frame can we expect legislative changes to help insurers to reduce litigation costs and amount of claims? When price increases are already in effect, do we have enough time to see rapid improvement of both sales and results simultaneously?

7 Conclusion

We are looking at a company that has performed poorly in the last couple of years for the reasons highlighted above. Company’s financial success mainly rests in the hands of unpredictable weather events. However, the underlying business remains strong and some headwinds can turn their direction in the near future. Florida, which has been left behind by major competitors and leaving many smaller competitors suffering, could deliver outsized results for Universal - until the storm hits again.

The investment thesis rests on the following grounds:

Increase of revenues: Higher market prices will help to grow Universal’s top line and market expansion to other states not only reduces risks but increases sales.

Decrease of costs: Legislative changes are about to reduce the amount and size of claims. Potentially, the current hurricane season is milder so there will be less expenses in the near term. However, investors in Universal's stock should pay attention to the development of the company's costs and investment income.

Solid financials: In long term perspective the company has delivered steady growth of revenue, premiums written, book value and cash flow.

Multiple expansion: If the financial performance of Universal gets back to its historical levels and remains sustainable, there’s little reasoning why the company is valued significantly below its historical multiples.

Attractive dividend and payout: The high dividend forms a solid base yield that gives patience to wait.

Sources

https://www.nerdwallet.com/article/insurance/home-insurance-florida

https://www.valuepenguin.com/best-cheap-homeowners-insurance-florida

https://www.insurancejournal.com/news/southeast/2021/02/12/601087.htm

https://www.insurancejournal.com/magazines/mag-features/2021/01/11/596731.htm

https://www.insurancejournal.com/news/southeast/2021/06/01/616457.htm

https://www.insurancejournal.com/news/southeast/2021/03/19/606052.htm

https://www.insurancejournal.com/news/southeast/2020/09/10/581974.htm

https://www.insurancejournal.com/news/southeast/2021/03/17/605699.htm

https://falveyinsurancegroup.com/what-is-an-mga/

https://www.nasdaq.com/market-activity/stocks/uve/insider-activity

https://www.alliance321.com/top-homeowners-insurance-companies-in-florida/

https://wusfnews.wusf.usf.edu/economy-business/2021-06-23/big-changes-are-coming-to-homeowners-insurance-in-florida

https://app.neilpatel.com/en/traffic_analyzer/overview?domain=clovered.com

https://www.morningstar.com/stocks/xnys/uve/valuation

https://www.fednat.com/wp-content/uploads/2021/08/ITEM-B-FNHC-Q2-2021-Press-Release-FINAL.pdf

https://www.salary.com/tools/executive-compensation-calculator/sean-p-downes-salary-bonus-stock-options-for-universal-insurance-hldgs?year=2020

https://seekingalpha.com/article/4454771-adecco-universal-insurance-high-growth-stellar-balance-sheets-5-percent-plus-yields

https://seekingalpha.com/article/4396451-capacity-to-bounce-back-after-pandemic-universal-insurance-holdings

https://seekingalpha.com/article/4442804-universal-insurance-holdings-inc-uve-ceo-steve-donaghy-on-q2-2021-results-earnings-call

https://seekingalpha.com/article/4418599-universal-insurance-potential-for-solid-price-appreciation-mitigates-weather-related

https://www.valueinvestorsclub.com/idea/UNIVERSAL_INSURANCE_HLDGS/6537621913

https://climatecenter.fsu.edu/topics/hurricanes