⏩ Speedy thesis #10: Novotek and JRSH

Stocks that pay a dividend while you wait for capital appreciation.

Speedy thesis works as a starting point for investment research: presenting potential opportunities and helping readers to do further research on companies and stocks that fit into their own (dividend investment) strategy.

In the issue number ten, I have included two very different small-cap companies.

A | Novotek - industrial digitalization. Dividend yield 2.8%.

B | Jerash Holdings - contract apparel manufacturer. Dividend yield 6%

Regarding Novotek, I got a bit late with the publication of this post. Novotek published its quarterly earnings on the 18th of August and the stock rose rapidly. I opened a small position at a price of SEK 47.4 on the 4th.

A | Novotek ($NTEK)

🔑 Growth niche, profitable growth, hidden champion, GARP.

📉 Not a bargain, potential slow-down in demand, dual class share structure.

Listing: Stockholm, Sweden.

Novotek in a nutshell: Novotek delivers “Industrial IT and Automation solutions based on standard products and components. Novotek’s focus is production, ranging from automotive via water treatment to petrochemical”. In practice, Novotek resells digital products from companies such as General Electric, Emerson and PTC to industrial end users in nine countries in Europe. In Q1 2023 the company had 188 employees, up from 165 in the previous year.

Founded: 1986.

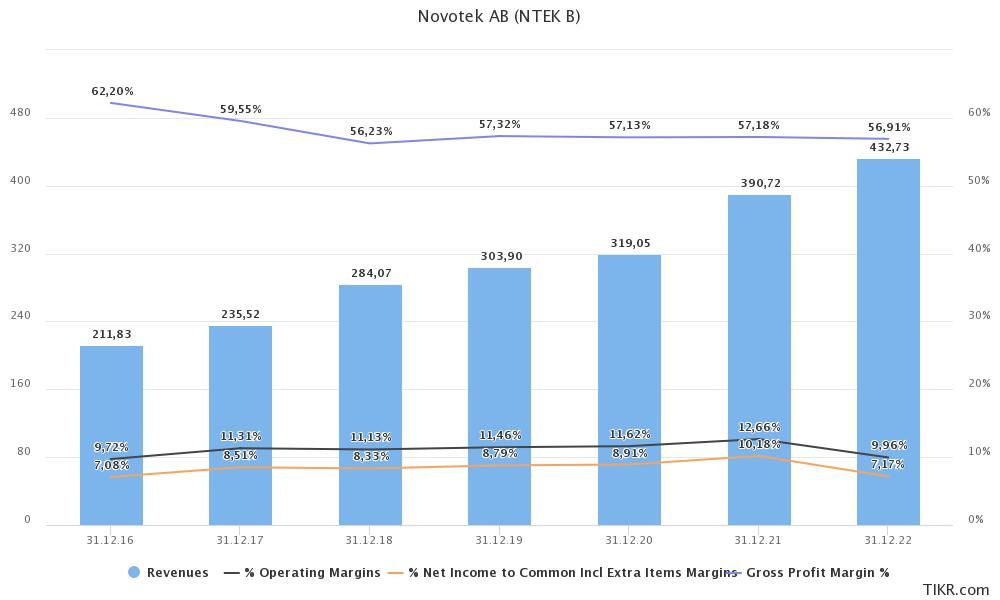

Investment thesis in brief: Novotek is a small-cap player in an attractive niche market. It has a strong track record of revenue growth while maintaining an excellent level of profitability. Due to the low capital requirements the business generates high returns on capital and cash flow. A fairly recent acquisition will drive the growth further and the financials are bound to benefit from weak Swedish krona.

Share price / Market cap: SEK 52.6 / 558 million.

Closest peers: IT-consulting companies.

Bull case 🐂

Business model: Novotek connects large industrial software providers with approximately 3000 customers annually (according to Analyst Group, source below). I believe its customers don’t have the internal expertise to meet the future requirements to stay competitive among the trends listed below.

Trends: All the buzzwords such as industry 4.0, cybersecurity, industrial automation and digitalization, IoT.

Competition: Novotek seems to primarily offer digital solutions of American companies. I would speculate that European companies such as Siemens, Schneider and ABB pursue to serve the customers directly in their home continent.

Excellent returns on capital: ROIC 21%, ROE 18-24% and ROA 7-10%.

Strong balance sheet: Net cash position.

Stable margins: GM 57-60%, EBITDA 10-13%, EBIT 9.5-13%.

Growth: Impressive revenue and EPS growth track record highlighted above.

Potential for acquisitions: In the end of 2022 Novotek acquired a British company working with same suppliers as Novotek. EV/EBITDA multiple of ~4x. Potential performance related payment will be due in 2025. This will increase the acquisition multiple to ~5x. The acquisition increased Novotek’s turnover approximately 8-10%.

Concentrated ownership structure: Novotek has a two share classes. A company called Noveko Syd Ab controls 44.2% of the voting rights. Individuals Annette and Fredrik Larsson control the company. They appear to be owners and working at a company called Idus, which provides industrial maintenance software. Fredrik sits on the board of Novotek. The second largest shareholder is Arvid Svensson Invest AB which has 24.9% of the B-class shares.

Committed senior management: Most of the senior management and especially the country managers have been part of the company for over a decade.

Weak Swedish krona: In 2022 only 15% of the revenues came from Sweden. 33% of the revenue were denominated in euro. This will likely boost results in the short term. 53% of the revenue came from Denmark, UK&I, Switzerland and Norway in the order of magnitude. The largest markets for the company are Benelux and Denmark.

Valuation💰

LTM P/E 22.5x, NTM P/E 18x. All of the peers are trading at higher multiples. That hasn't been always the case in the past decade.

EV/EBIT of 9.4x sits slightly below the 5-year average of 9.8x.

EV/FCF 10x with free cash flow margins typically at around 10%.

Dividend yield 2.6 %. Payout ratio 59%.

There doesn’t appear to be analyst coverage on the company anymore, thus no target prices.

Bear case 🐻

Valuation: Novotek is not particularly cheap. The stock is trading near its historical averages. Considering the track record of the business the valuation is representative of the quality characteristics of the company.

Demand slow-down: One of the main questions is if the industrial companies will curb their investments into digitalization. Novotek states that the level of interest to the solutions remains high, but decision processes are longer. This has been a common theme among IT-consulting companies across the Nordics.

Competitive advantage: Consulting companies generally speaking have rather limited moat, but Novotek could possess some level of stickiness since it taps into the mission critical processes of the customers and changing a supplier, advisor and constultancy could present a larger risk for the customer.

Cost base: A large chunk of Novotek’s cost base is personnel costs, which in case of high wage growth could pressure the margins. Most likely, Novotek doesn’t possess much of a negotiation power over its software suppliers.

You can find Analyst Group’s sell side analysis over here - however it’s from 2020.

Good overview of the financials and multiples over here.

Summary: Novotek demonstrates many characteristics of a high quality company with excellent track record. It’s recent quarterly earnings were strong with all the key figures developing positively. Also, the order back log grew in spite of customer’s prolonged decicion making.

B | Jerash Holdings ($JRSH)

🔑 Onboarding of new customers, solid balance sheet, trading 0.6-0.7 times tangible book value, high dividend, concentrated ownership.

📉 Customer concentration risk, low returns on capital, potential personal vehichle for the CEO and main shareholder, uncertainty about the duration of the weakness of the demand.

Share price: $3.35.

The summary below is generated by Chat GPT from my analysis, with quite a few modifications.

Bull case 🐂

Resilient growth: Jerash Holdings, a contract apparel manufacturer, has historically achieved low-teens sales growth and maintained a solid balance sheet.

Diversification initiatives: The company is actively reducing customer concentration by onboarding new clients like Hugo Boss through joint ventures and expanding production for brands like Skechers and Timberland.

Deglobalization advantage: Jerash is well-positioned to benefit from deglobalization trends, as brands seek to diversify their supply chains away from Asia, potentially driving increased business.

Market recovery upside: As apparel sales normalize post-pandemic, Jerash's strong competitive advantage, including free trade agreements, could lead to significant growth and earnings potential, when apparel brands move their production out of China and Asia.

Attractive valuation: The stock currently trades at a historically low price relative to sales, assets, and earnings potential, with potential for a rebound in share price as market conditions improve.

Bear case 🐻

Industry volatility: Jerash operates in the apparel manufacturing sector, which has experienced turbulence due to pandemic-related disruptions and overstocking by retailers.

Customer concentration: The company's heavy reliance on one major customer, V.F. Corporation, poses a significant risk to its revenue stream.

Operational challenges: Jerash faces quarterly fluctuations in business due to order postponements and product mix changes, impacting revenue and margins.

Geopolitical and trade risks: The company's operations in Jordan expose it to geopolitical risks, and the fragility of trade agreements could impact its cost advantage. The imposed taxes on the company has been recently on the rise reducing its net income.

Valuation pressures: The uncertain industry outlook and soft demand will most likely remain an issue for the next 12-18 months. Therefore the investment case is not

My target price for the stock is at around $5.4, which expects the net income to return to slightly below historical levels, moderate growth and earnings multiple of 9x, below the average of 10x.

My analysis on Seeking Alpha for more information. JRSH 0.00%↑

My twitter handles

🇬🇧 English: @paidwait

🇫🇮 Finnish: @anttisleinonen

Overview of previous publications

Notes

I’m considering entering back to Mondi, which I sold before the H1 trading update. The business was soft similar to other companies in the pulp, paper and packaging sector. The move was lucky one.

Relais has traded back to the levels where it made big upswing. This could be a point where to increase the position. The Q2 earnings were OK and the company made yet another acquisition in Norway.

I’m considering adding to Dun & Bradsheet which had a decent Q2 and seems to be going to the right direction. DNB 0.00%↑