IHS Holding: Telecom towers thrown to trash?

Quick value idea from telecommunications infrastructure sector.

Ticker: IHS

Stock price at the time of writing: $11.4.

Summary

Communication tower company IHS Holding made an unsuccessful IPO in October 2021 and the shares have been in heavy decline since then.

IHS is one of the largest international tower companies operating in Africa and Latin America, with a high concentration of towers in Nigeria.

IHS has room to develop and grow its business, and it has recently closed significant acquisitions to diversify its asset base.

When looking at the business performance, analyst estimates, peer evaluation and finally recent comparable deals in the industry, IHS shares could have significant upside potential.

Introduction

For a long time, communication tower companies have been darlings of the REIT industry. American Tower, the largest listed tower company, has returned nearly 300% during the last 10 years. Communication towers have been hot merchandise not only in stock exchanges but also among private equity investors and asset managers.

Mobile network operators (MNO) have taken advantage of this continuously growing interest, as mentioned in the previous sector review. MNOs have been disposing their tangible assets into separate companies, selling the assets to different kinds of asset managers, such as Brookfield, or independent tower companies, such as IHS Holding or American Tower. The industry has gone through a period of reorganization and consolidation, and will likely continue on this trajectory.

Today the most well known tower companies come with elevated valuations. For a value investor it doesn’t do harm to look left and right for alternatives. One of them is IHS Holding. Although IHS was listed just recently, it has a decade-long operational history starting in Nigeria in 2001. Since then, the company has expanded to two continents, nine countries and over 30 500 telecommunication towers, making it the third largest international tower company.

A recent IPO on a slide

Since its debut as a listed company, IHS shares have been on a downward slide. The company IPO’d in October 2021 with a price range of $21-$24 and the shares commenced trading at $21. Right away the share price slipped down to 17 dollars. By Christmas 2021 the shares were trading between $13-$14, down about one third since its first day of trading. At the time of writing, the shares have lost nearly half of the value in the IPO. In the short term, this can be viewed as a failed public offering. During the past couple of months the U.S. listed tower companies have also experienced a correction, but IHS has been in its own league.

Share price development of IHS and U.S. listed tower companies. Source: Seeking Alpha.

The ownership of the company is rather concentrated. MTN, largest MNO in Sub-Saharan Africa and largest customer of IHS, holds approximately 25% of the shares. MTN has expressed that it will dispose of its holding in IHS over time, but supposedly hasn’t yet done so. It is expected that MTN will be reducing its holding, due to the fact that MTN sold its tower assets to IHS in order to lighten up its own balance sheet. The second largest shareholder is Wendel, a French private equity investor, with 23% ownership in the company. One of the founders of IHS, Sam Darwish, still has nearly 3% ownership in the company.

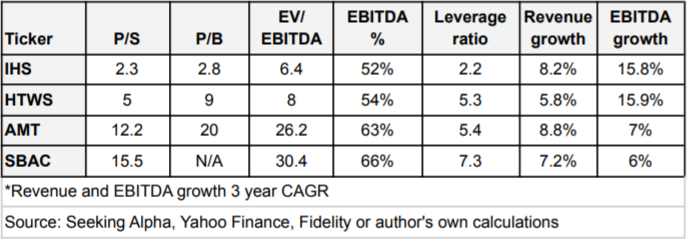

Before looking at the valuation of IHS and its competitors, it’s important to note that IHS Holding and Helios Towers (HTWS) are limited companies. American Towers (AMT) and SBA Communications (SBAC) are both REITs and include other assets than free-standing telecommunication towers, which makes comparison of some valuation multiples not so straightforward. In addition, this means that IHS will not be included in ETFs that focus on REITs. As REITs both AMT and SBAC pay a modest dividend, IHS does not pay a dividend and neither intends to. This will naturally limit the interest from dividend investors.

Mysterious valuation

Wall Street analysts see much more value in IHS than the market does. According to Seeking Alpha the average target price is $24.33, lowest being $21 and highest $29. In total there’s six analysts following the company. The current share price hovering around $11-$12, this represents 100% upside to the estimates of the analysts. All of them have a buy rating on the stock. Since analysts are more often wrong than right, there’s no reason to make an investment decision solely based on target prices.

Peer analysis makes the valuation picture especially interesting. Closest listed peers of IHS are American Tower, SBA Communications and Helios Towers, which is listed in the London stock exchange. Both AMT and SBAC have significant exposure to developing markets. Helios Towers tower portfolio is fully located in Africa and the Middle East. IHS has most of its towers in Africa, only 13% of them are located in Latin America.

Comparing IHS to American Tower, which has 77% of its towers outside of the United States, can make investors scratch their heads. Both of the companies generate the same amount of revenue per tower. AMT makes 23% more EBITDA per tower, partly explained by higher tenancy ratio. However, the market cap per tower of AMT is 5x higher and enterprise value per tower is 4.6x higher. This difference in valuation gives AMT rather elevated multiples, whether we look at P/S, P/B or EV/EBITDA.

Although both AMT and SBAC have a more geographically diversified portfolio of towers and higher level of profitability, their valuation greatly exceeds the valuation of IHS when looking at indebtedness and growth of revenues and profitability. IHS scores better in almost every respect. It carries a lower level of debt, historical revenue growth matches its competition. EBITDA has grown at a significantly higher pace than more richly valued incumbents. The lower EBITDA margin gives a reason for a small discount.

The valuation of IHS can also be viewed in proportion to comparative deals made in the industry, often valued in between 12x-17x EBITDA multiples (Source), in the African continent lower than in Latin America. American Tower completed its purchase of Eaton Towers in 2020. The EBITDA multiple the company paid for 5700 towers in Africa was approximately 13x (Source). Since communication towers are relatively uniform and there’s little differentiation, it is difficult to argue why IHS should be trading at significantly lower multiples.

Their towers are not trash

Trends driving the business of IHS are the same as for every other tower company. IHS has a handful of emerging market drivers that are likely to boost its business in the long term. For example, the increase of smartphone users will drive data usage in developing markets. The growth of emerging markets is also visible in the Q3 2021 results of American Tower, which reported significantly higher growth rates for Africa and LatAm regions than for developed markets.

Compared to the tower companies in developed markets, IHS has still room to grow its ratio of co-location, meaning how many tenants occupy its existing towers. This is the same path that American Tower took to increase its funds from operations over the years of international expansion. Currently IHS has on average 1.5 tenants in a tower, when the average co-location ratio of independent tower companies was 2.4 in 2020 (Source).

Major cost component of IHS operations is the fuel that powers up the equipment of the telecommunication tower. The rising price of diesel will place pressure on its earnings due to the fact that the cost of diesel represents nearly 30% of IHS’s revenue. The price of diesel is likely to rise faster than IHS’s annual rent escalators. Currently, 45% of its towers are powered up by hybrid solutions, combining renewable energy and diesel generators. In other words, there’s large potential to reduce fuel costs and increase ESG merits of its operations.

During the past four months IHS has been working hard to acquire new assets. It has closed a deal to acquire TIM Brasil’s fiber assets in Brazil, 5700 towers in South Africa from MTN and made an agreement to build 5800 towers in Egypt in the following three years. Just recently IHS purchased 2100 towers in Brazil. These examples show that there’s plenty of room for growth, in the United States independent tower companies own 90% of all telecommunication towers, whereas 42% and 55% of the towers in Sub-Saharan Africa and in Latin America respectively are owned by independent tower companies (Source).

What could go wrong?

No investment comes without risks. One of the reasons for lower valuation of IHS could be its concentration in the most populous country of Africa, Nigeria. Approximately half of its towers are located in the country, in 2020 74% of the company's revenues and 85% of EBITDA are generated in Nigeria. Today, American Tower and IHS compete head to head in Nigeria, where AMT has a market share of 32% and IHS has 44%. Allegedly, Nigeria represents high risk of issues with repatriation of earnings. In order to diversify its tower portfolio, IHS needs to find and acquire assets in other regions - succeed in its growth strategy.

IHS also has significant customer concentration, 65% of revenues generated by MTN (55%) and Airtel (10%) accounts. Remembering that MTN has a significant ownership in the company, there’s a potential conflict of interest whether MTN will act as a customer or as an owner. Especially in Latin America, consolidation of mobile network operators has reduced the total need for communication towers. Operating in developing nations will always pose a risk of currency depreciation. 64% of IHS’s rental income is nominated in U.S. dollar or euro. This leaves a part of the revenue stream vulnerable to exchange rate fluctuations.

Conclusion

The price decline of IHS has gone too far in many respects. The fundamentals behind IHS business are strong and the characteristics of its business model provide a high level of reliability. Despite the potential overvaluation of many other tower companies, currently the valuation of IHS stock has too large gap to its peers. Also, an isolated look at valuation multiples of IHS, will represent a rather fairly valued and growing company in emerging markets.

When considering an investment in IHS, one has to remember that IHS is a newly listed company and therefore most of the investors are unaware of its merits and even existence. Together with concentrated ownership structure, a growing interest from institutional investors can mean tailwind to the stock price. Even if IHS would only lift itself up to the multiples of Helios Towers, there’s a significant upside potential.

The current price represents a good opportunity to open a starter position in IHS and add to the position if the company proves itself in the coming quarters and draws investor attention. Both analyst estimates, private market deals and public market peers point out that IHS could have 100% upside potential.

Catalysts for higher share price

Small free float.

Reversion to the mean.

Re-rating of the valuation.

Further diversification from Nigeria.

Reduced selling pressure on recent IPOs.

Inclusion to EM and infrastructure funds.

Higher investor interest in companies operating in emerging markets.